Imagine a racetrack with 10 horses. The first two horses (NFLX and DIS) are peeling away from everyone else; with NFLX still having a sizeable lead over DIS. But the stage is set for DIS to start accelerating faster than NFLX. This is how I would describe the US Media sector today, and Disney’s Q1 results released yesterday only serves to bolster that narrative.

One of the major reasons why I haven’t really done a lot of quarterly earnings reviews in the past is because editing articles is actually a major time-sink. Since editing adds relatively insignificant value next to actual equity research, I haven’t been able to justify doing quarterly earnings reviews before.

However, doing quarterly earnings reviews becomes more feasible if I do them in a disorganized “chat format” like this, and in a more casual conversational fashion, as it involves little editing. Going forward, I’ll also be looking into how AI can help me further save editing time. So look forward to more abridged quarterly earnings reviews of this variety.

Without further ado, here’s a review of Disney’s latest Q1 results:

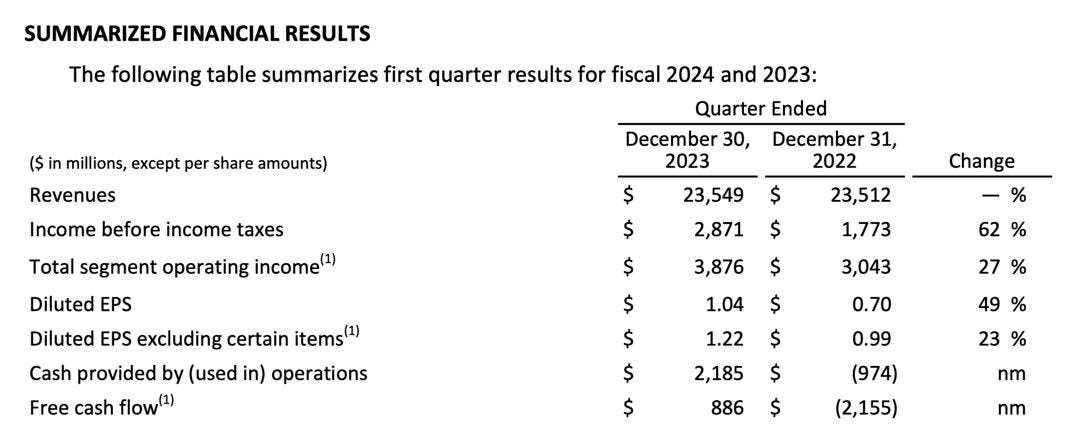

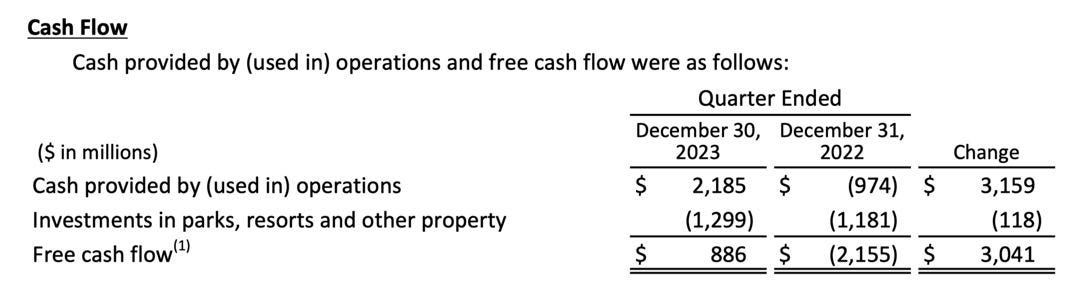

YoY improvements in Q1 were mostly due to lower costs. This also resulted in higher FCF, back to positive territory.

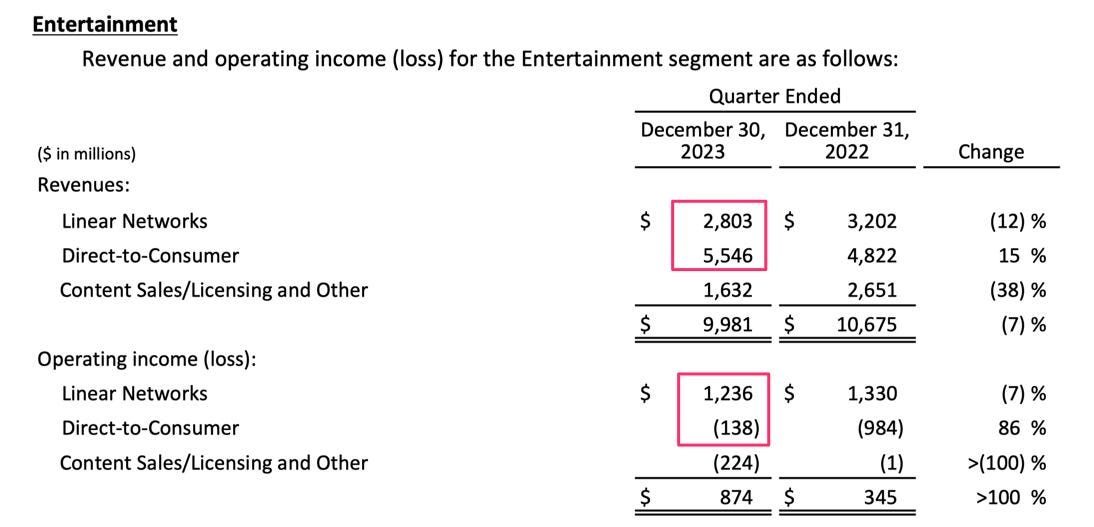

For simplicity's sake, just focus on the right column 'Change' YoY. Nothing material here in a normalized extrapolation sense. Entertainment Op Inc did improve materially, but not very insightful for normalized forecasting.

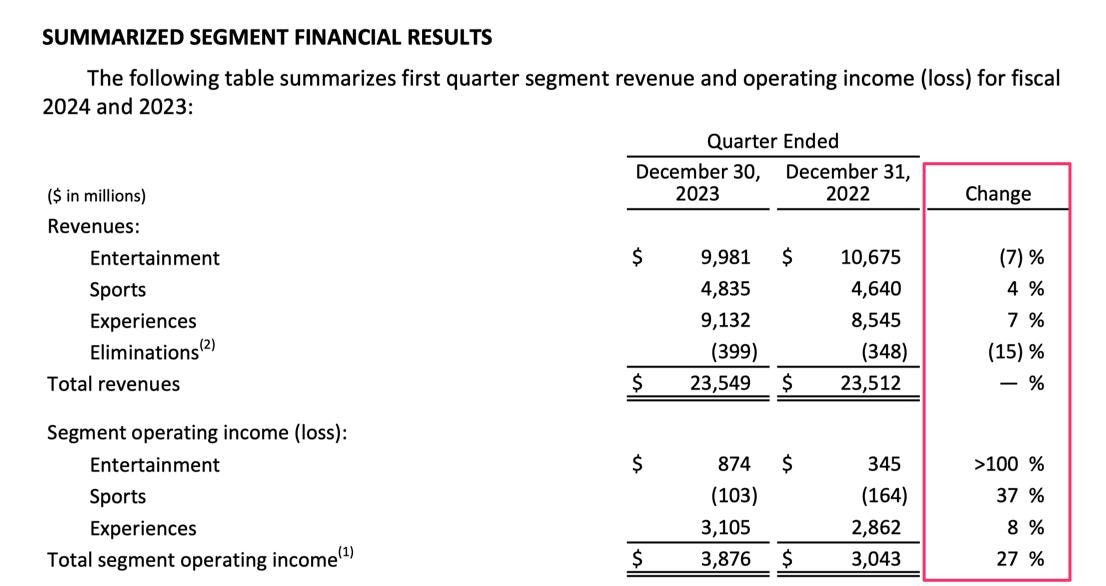

Seems like DIS is balancing the melting ice cube transition from Linear to DTC just fine, both in terms of Rev and OpInc.

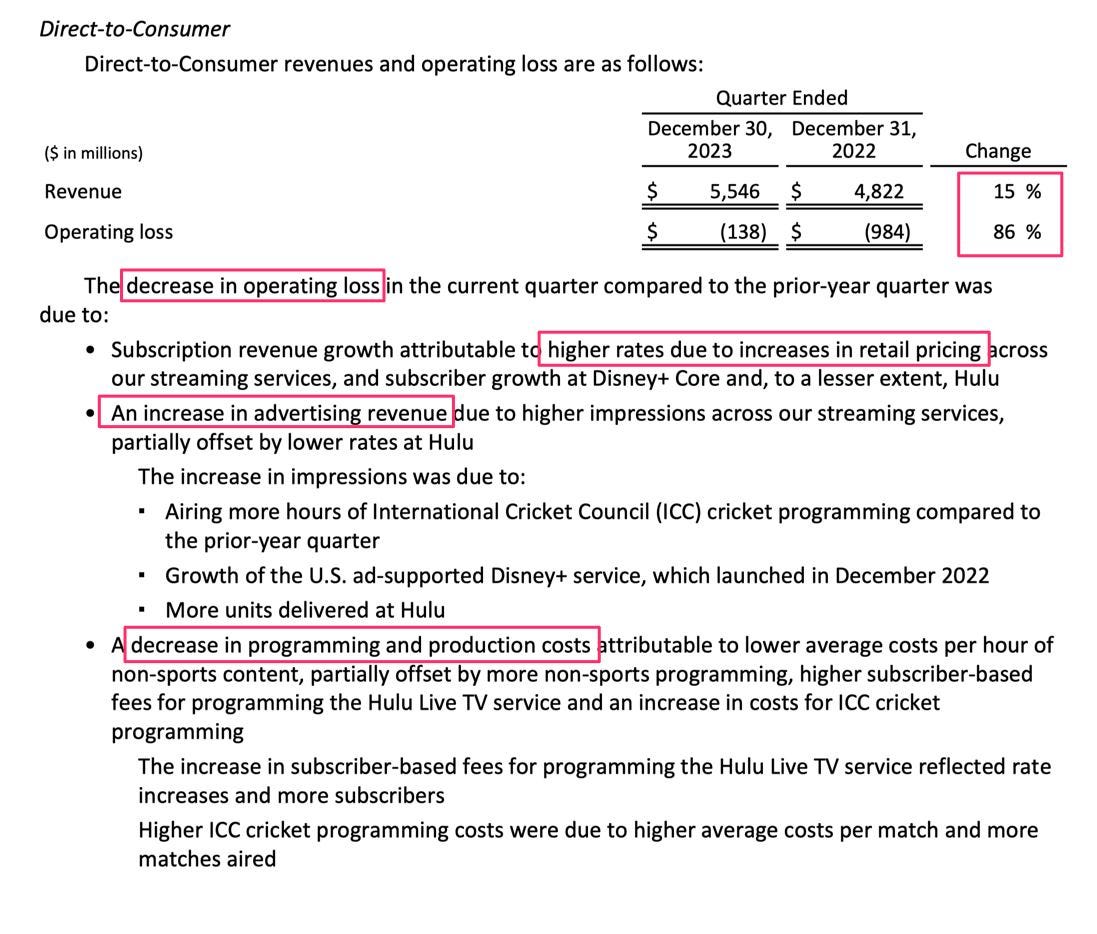

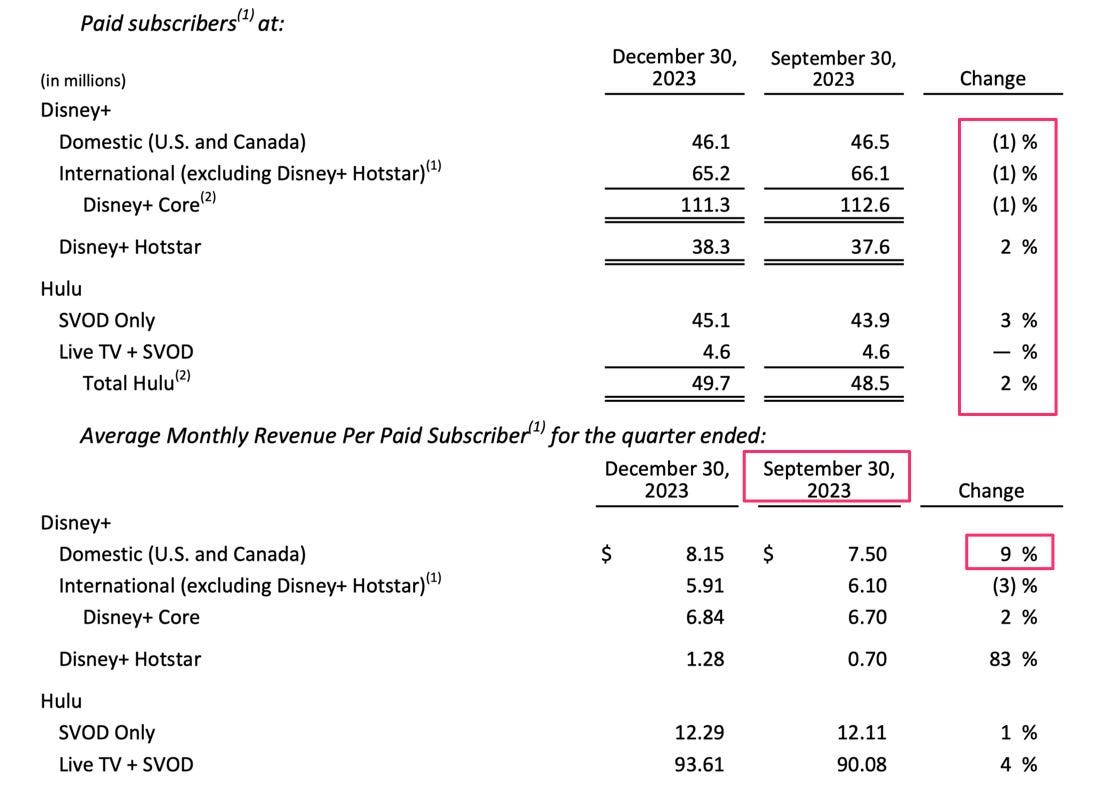

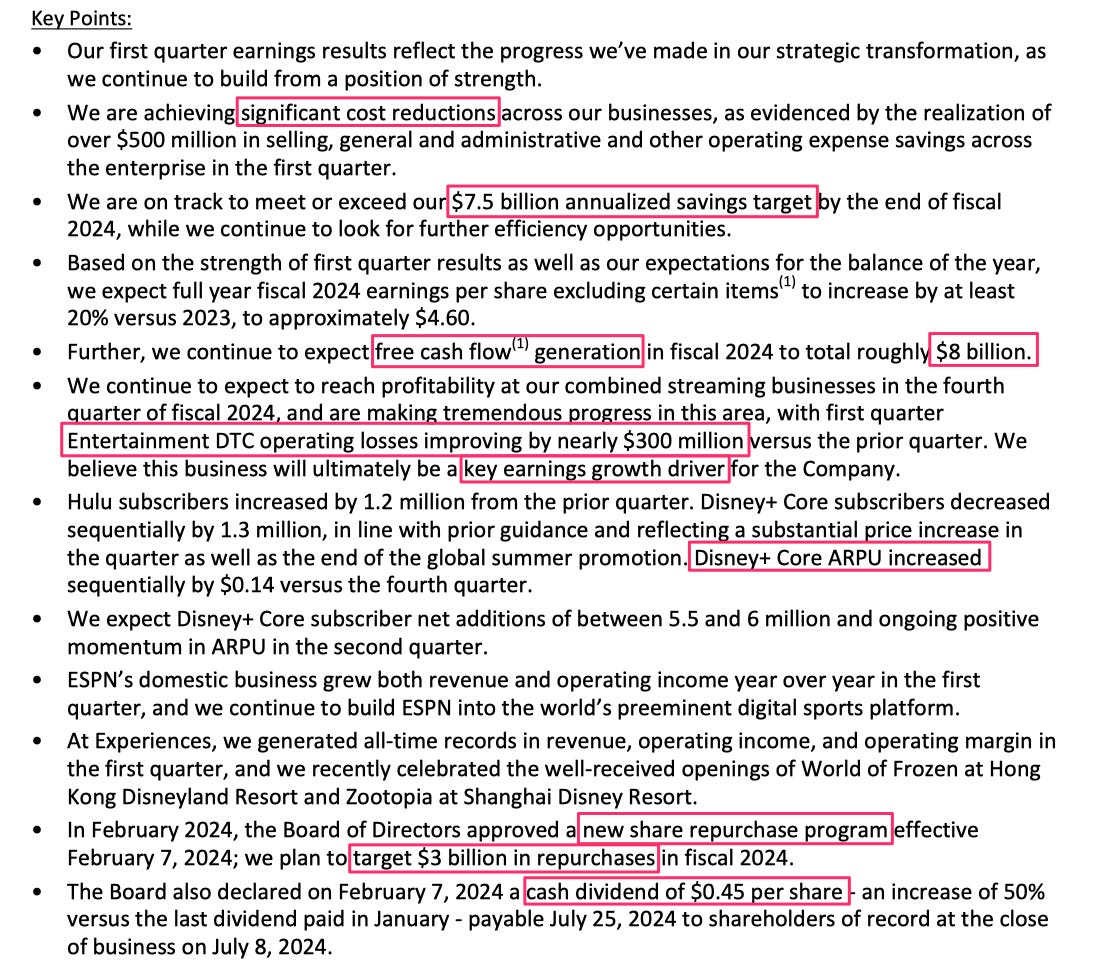

Q1 factors behind DTC improvements YoY

DTC subscriber volume saw no significant changes YoY. Increases in unit DTC prices were the main contributor of DTC improvment. Notice that the 9% price hike is based on sequential changes QoQ, not YoY. For context, UCAN unit pricing is by far the highest of all geographical segments.

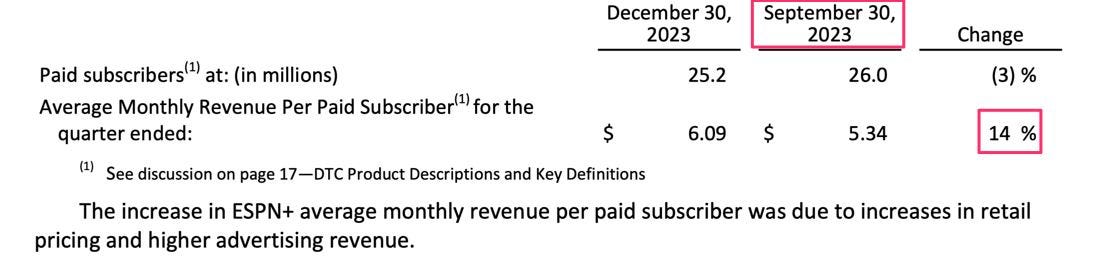

Sports DTC is still growing from a relatively small base, so not yet outsized contribution to Group level. But sequential price hikes QoQ is massive at 14%.

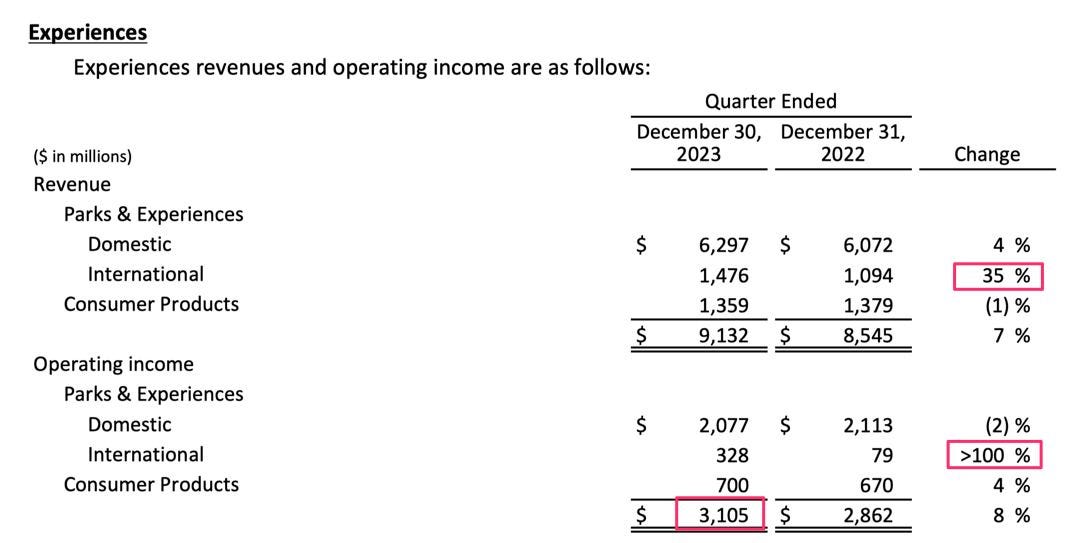

Parks incremental contribution YoY mainly came from improvements in International.

Reductions in DTC losses and tightening of operational efficiencies contributed to higher Group cash flows.

Other Q1 highlights

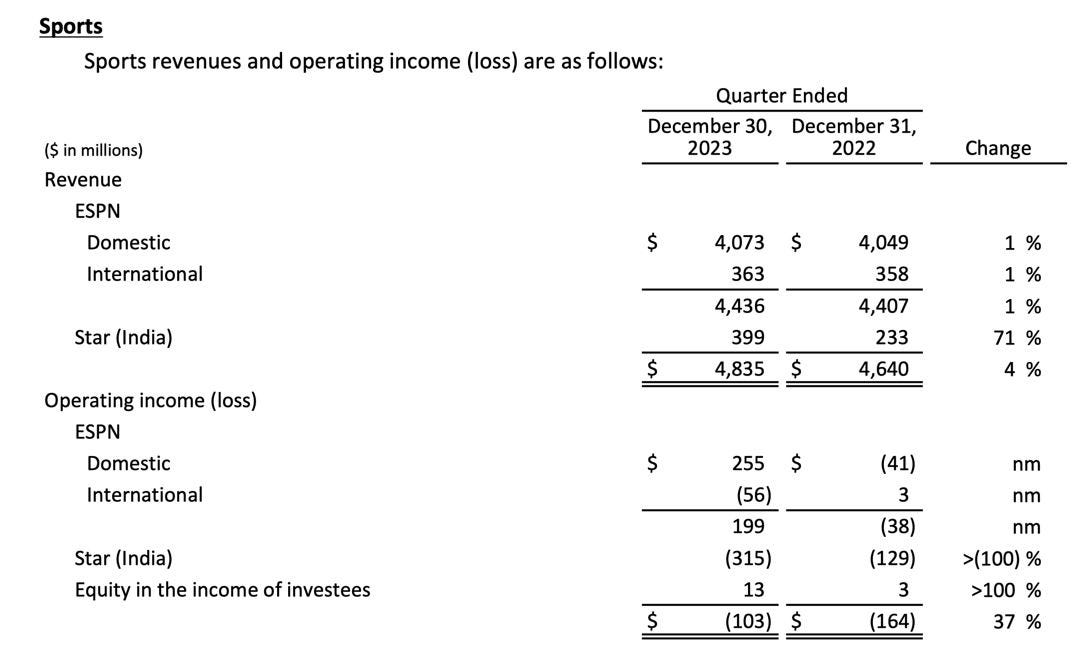

Given the new ESPN partnership between Bob Iger (DIS), Rupert Murdoch (FOX) and John Malone (WBD), it is unlikely that NFLX will be able to incrementally grab much more broadcasting rights of sports majors from the incumbents.

No material financial changes from previous quarter. The new developments are well within expectations, as previously discussed in my Disney reports (links below). I’m intrigued to see what else comes out from their new Sports partnership.

Great read. When I wrote my piece on how Netflix had won the streaming wars last month I was hopeful for Disney to show some life. They definitely have with this recent earnings call. This is a nice breakdown of it.

Disney is such an interesting company for a deep dive. If I had boundless time, it would be one of the companies I'd follow and study regularly. It's a little like a slightly more synergized Berkshire, in a way.

The video game news is notable and very interesting, but the market's reaction is a little bit of a surprise. It's not like this wasn't cooking already, but maybe the speed at which the deal materialized has given some investors hope.

Great read. When I wrote my piece on how Netflix had won the streaming wars last month I was hopeful for Disney to show some life. They definitely have with this recent earnings call. This is a nice breakdown of it.

Disney is such an interesting company for a deep dive. If I had boundless time, it would be one of the companies I'd follow and study regularly. It's a little like a slightly more synergized Berkshire, in a way.

The video game news is notable and very interesting, but the market's reaction is a little bit of a surprise. It's not like this wasn't cooking already, but maybe the speed at which the deal materialized has given some investors hope.