AGCO: If META Sold Luxury Tractors (Part 3)

2x Sector Growth by 2029: 1st-mover innovator addressing new TAM under a highly differentiated business model (modular, open-source)

Executive Summary:

AGCO represents an incredibly unlikely high-growth innovation story in the Ag sector, with clear and ambitious operating targets to be achieved by 2029. The world’s No. 3 AgEq supplier after Deere and CNH presents a masterplan to penetrate the lucrative North American market, by targeting historically untapped farmer segments and reimagining the legacy dealership model. Its dedicated mixed-fleet approach to high-growth Precision Ag lays the foundation for a differentiated value proposition which its competitors are unlikely to replicate, and enables previously unconceived sector operating models. AGCO’s base-case valuation supports the existence of substantially asymmetric risk:reward — whether it achieves its highly ambitious operating targets or not.

Unlike CNH’s largely macro-driven growth in Part 2, AGCO’s fundamental-based growth is very much business-driven and within management’s control. Hence, this AGCO analysis in Part 3 is not a rehash of the largely macro-driven CNH analysis in Part 2. Instead, it will build on the Ag + AgEq sector outlooks found in both Parts 1 & 2 and focus on analyzing AGCO’s fundamentals purely from the bottom-up.

TABLE OF CONTENTS:

1. AGCO: Historically Outperformed Deere & CNH

2. Big 3: Not The Same

3. AGCO LT Outlook: High-Growth Innovator

4. AGCO 2025: ST Outlook

5. Asymmetric Valuation: Base-Case & Bear-CaseBloomberg Interview: AGCO CEO Sees 2025 as the Bottom of the Farm Slump

Interview Summary:

AGCO's CEO anticipates 2025 as the bottom of the current farm industry slump, citing positive indicators despite a 2024 downturn. The CEO downplays tariff impacts on AGCO directly, but expresses concern for potential effects on crop demand and farmer profitability. AGCO's strategy to counter industry cycles centers on "smart farming" through advanced technology in machinery, aiming to boost output while minimizing input. Significant investments in R&D and strategic partnerships are driving this. The company is also focused on expanding its high-end Fendt line to gain market share in North and South America, emphasizing its technology and farmer satisfaction.Click here to read full transcript

AGCO: Historically Outperformed Deere & CNH

Summary:

AGCO has demonstrated historical outperformance compared to CNH and Deere, with a 10-year average net margin of 5% similar to CNH's. Its capital allocation and asset turnover ratios exceed peers' averages by 2x, while its ROA edges out even the larger Deere's. Deere's trailing P/S ratio stands at a significant 4x premium over AGCO and CNH.AGCO has demonstrated historical outperformance as compared to both CNH and Deere. Its 10yr average Net Margin of 5% over a full-cycle is similar to CNH’s — even though both Deere and CNH have almost 10x higher average gearing than AGCO:

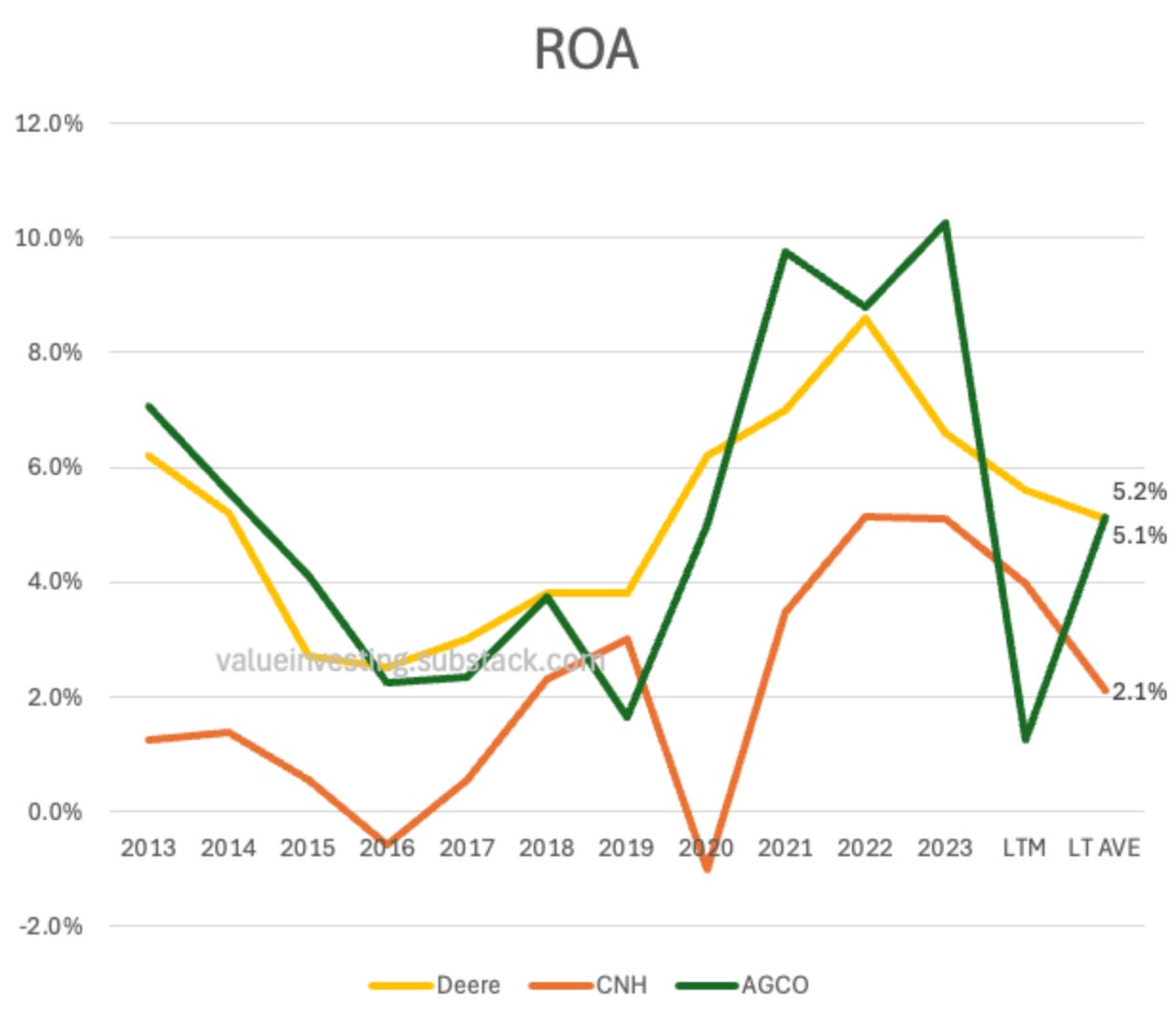

AGCO also vastly outperformed its peers in capital allocation. Its 10yr average Asset Turnover (over a full-cycle) was over 2x both of its peers; and it even manages to edge out the 10yr average ROA of the larger Deere (with greater economies of scale):

While intuitively this could be attributable to AGCO being a smaller business than both CNH and Deere, the latter two should have benefitted from greater economies of scale, thus somewhat offsetting the former advantage. Hence, AGCO’s unit outperformance here seems to be genuine.

As indicated earlier, AGCO has significantly more room to increase its financial leverage. This can be demonstrated by AGCO’s similarly superior 10yr average ROIC below, despite its far smaller economies of scale:

This led me down a rabbit hole to investigate the reasons behind AGCO’s superior outperformance. The performance drivers behind AGCO’s and CNH’s businesses are actually very different, with AGCO’s growth being largely fundamental-based while CNH’s growth is more sector macro-based. So rest assured that this AGCO deep-dive is not going to be a rehash of the preceding CNH report in Part 2.

The main reason why I’m not analyzing Deere in this report is because it has significantly higher trailing multiples, both in terms of P/E and P/S. AGCO’s trailing 0.6x P/S is similar to CNH’s 0.7x. By contrast, Deere’s trailing P/S is 2.5x (4x higher).

I’m using P/S here because of AGCO’s artificially high trailing PE owing to the prevailing Ag downcycle. Also, those interested in analyzing Deere can simply start from my earlier CNH analysis in Part 2 and make adjustements from there, since their businesses bear more similarities

Big 3: Not The Same

Summary:

AGCO's outperformance compared to peers may be due to its non-overlapping market segments with Deere and CNH, each targeting distinct value propositions. Deere's "walled-garden" approach to its AgTech favors large farms with full Deere tractor fleets. CNH offers a mid-tier option with a more flexible approach to AgTech, but has faced integration challenges due to its "hands-off" approach to mixed-fleet configurations. AGCO provides premium Fendt tractors with a dedicated mixed-fleet dealer network, supporting smaller farmers' incremental adoption of 3rd party AgTech solutions. This reduces the entry barrier to Precision Ag and allows smaller farms to enjoy greater yields at lower upfront costs ($20,000 vs $1M).

Perhaps one reason for AGCO’s outperformance relative to its larger peers (Deere and CNH) is because it doesn’t compete head-on with them. The Big 3 AgEq suppliers each represent different value propositions to farmers, hence targeting somewhat non-overlapping market segments:

Deere

Known for being the expensive turnkey supplier. It has a “closed-source” approach to Precision Ag, enforced by having them factory-installed in their tractors. This means farmers cannot gain access to Deere’s AgTech without a Deere tractor, but it also makes activating solutions as simple as signing up for a subscription. This makes Deere the equipment supplier of choice for large farms with entire Deere tractor fleets, but puts off smaller farmers with existing mixed fleets or those who prefer to incrementally bolt-on equipment from different brands.

CNH

Known as the mid-tier, more affordable option — but has a somewhat clumsy approach to Precision Ag. CNH practices a “mixed-fleet” approach, which allows 3rd party AgTech solutions to be bolted onto their tractors. This naturally excludes larger farmers with existing full Deere fleets, making it a closer competitor to AGCO. However, the lack of any dedicated mixed-fleet support makes configuring different equipment brands to work together somewhat of a jigsaw puzzle, which has introduced integration challenges in Precision Ag.

AGCO

Best known for their premium Fendt tractors. AGCO not only practices a mixed-fleet approach, it’s building a dedicated mixed-fleet dealer network tasked with supporting mixed-fleet configurations. This means that a small farm can incrementally bolt-on 3rd party AgTech solutions to their existing tractors, significantly reducing the entry barrier to Precision Ag. Some of these only start at only $20,000; in contrast to having to buy an $1M Deere tractor just to enjoy the benefits of AgTech. This allows smaller farms to immediately enjoy greater yields from Precision Ag without having to break the bank.

While they are most definitely competitors, each of the Big 3 appear to deliberately focus on different market segments to cultivate differentiation. Each of their current market focuses demonstrates relatively low overlap — thus implying relatively low competitive intensity between the Big 3. This implies that AGCO isn’t at a serious competitive disadvantage relative to Deere or CNH despite being smaller.

Ambitious Targets To 2x Sector Growth By 2029

Deere’s roughly 10x larger market cap ($130B) implies a much larger business than CNH ($16B) or AGCO ($8B). However, Deere’s trailing revenues are actually only 2.5x larger than CNH and 4x larger than AGCO. Their total revenues are also not apples-to-apples comparison — AGCO is an Ag pure-play, while both Deere and CNH have Construction business segments.

Keep reading with a 7-day free trial

Subscribe to Value Investing for Professionals to keep reading this post and get 7 days of free access to the full post archives.